It’s funny how there are some myths you know by heart, even if you can’t remember where you heard them first. Eating your crusts makes your hair go curly, carrots are good for your eyesight and if you’re pulling a face while the wind changes, it will get stuck like that.

(Actually, I do remember where I heard these. My mom has a lot to answer for.)

Well, those kinds of myths aren’t just reserved for moms trying to make you behave – they exist in the world of personal finance too.

But don’t worry – you’re not doomed to fall victim to these money myths for much longer, because I am here to dispel them once and for all… or 7 of them, at least.

Carrying a credit card balance helps you build up a credit score

Ugh. If I never hear this again, it will be too soon. There’s been this pervasive myth for years now that in order to build up a credit score, you need to carry a small balance on your credit card from month to month.

While yes, technically, carrying a balance will leave you with a nice lengthy credit history, but it will be a bad one. This myth has been thoroughly debunked by now and the only thing you’ll get from carrying a balance is a big bill and a black mark on your credit score.

Just pay your credit card bill in full, each and every month, ok? Ok.

A credit card can replace an emergency fund

Uhhh, what? The idea that you don’t need an emergency buffer because you can just put that unexpected fine, last minute flight or emergency replacement iPhone on your credit card is baffling to me.

Look, a credit card can be super useful tool to manage your spending and budget – but charging large amount on it in an emergency should be your worst case scenario, not your first plan of attack. The last thing you need if you’ve taken an unexpected hit to your budget is to wind up with a big interest bill on top.

If you possibly can, it’s far better to start squirreling little bits away to build up a savings buffer and leave the credit card for expenses you know you can pay off within a month. And if you really want to give this “Adult” thing a red hot go, make sure you avoid these these other common credit card mistakes while you’re at it.

Only one person in a relationship needs to look after the finances

This attitude spells trouble with a capital T. There are numerous glaring problems with letting one person take on all the financial responsibility, not least of which is, what happens if you break up? I know that’s not a pleasant thought, so let’s table that and look at it a different way: is it really fair to your partner?

If your partner holds the purse strings, they’re the one facing down bills each month, frantically running the numbers in their head at the checkout, and being the one to say “sorry, but we can’t afford that.” It’s no fun to be that person, and it probably won’t win them any points with you either, if you’re honest with yourself. It’s much better for everyone involved if you both share the responsibility – you know, like functioning adults.

Investing is only for rich people

Ok, I’ve fallen victim to this one in the past. The sharemarket sometimes seems like a nerve-wracking place, reserved for the kind of ridiculously rich people who could shrug and laugh if they made a bad call and lost $50,000 in one fell swoop.

But this isn’t actually true and you shouldn’t let it stop you from getting involved – investing can be easier than you think, and it’s a great way to diversify your income streams. Plus, let’s be honest, with interest rates the way they are, your money isn’t doing a whole lot of good sitting in a savings account – it might as well be working harder for you.

If you don’t have the time or inclination to get involved with the sharemarket, there are other options like becoming a peer-to-peer lender. So no excuses.

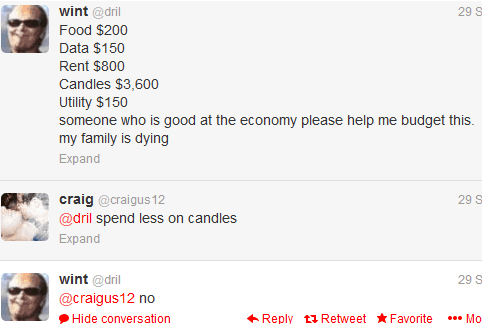

Tracking your spending is the same as a budget

Uh, no. It’s not. Tracking your spending is looking backward, and saying, “I spent $80 on cold pressed juice this week, now how will I pay for that festival ticket?” A budget is looking forward and saying “I want to buy a festival ticket, so this week, I will not spend $80 on cold pressed juice.”

Ok, so that’s a very (personal, embarrassing and) narrow example, but what I mean is that a budget is planning for the future, so that you’re making the most of your money, not just keeping an eye on where it all goes. A budget is about taking action, not just passively watching your money as it exits your bank account and passes you by.

An example of @dril tracking spending instead of budgeting.

All debt is horrible and scary

I’ll admit, my knee jerk reaction to being in debt is mild panic and a burning desire to get out of it ASAP. But part of growing up and becoming financially savvy is recognising that there’s such a thing as good debt and bad debt. Good debt is a mortgage that means you eventually own your own home, bad debt is a credit card bill that means you wake up in a cold sweat most nights.

And I know, I know – after the Global Financial Crisis we all developed a well-honed (and arguably perfectly reasonable) aversion to debt. But conquering this fear will help you move forward in your financial life and tackle big milestones like buying a car, or a home or taking a much needed backpacking trip to Europe to discover yourself.

Loaning money to your loved ones is a good thing

You might not think finance is a particularly emotional topic – but you’d be wrong. People get touchy when it comes to money, and that’s why lending your cash to family and friends rarely works out well. The last thing you want is to have a falling out with your best friend since forever because they still haven’t paid you back from when you lent them the money for an emergency flight home.

While it might seem like a kind thing to do at first, the obligations and emotions around lending money mean you’re better off leaving it to the banks. Or go ahead and give your brother the $800 he needs to fix his death trap of a car – but consider it a gift and wave it goodbye. It may be a gift that will be returned, whether in the form of money, favours or life-long gratitude and groveling, but don’t count on it.

She’s On The Money is the resident personal finance blogger over at mozo.com.au, bringing you the cutting edge of money matters, along with a side serve of good old fashioned dad jokes.

2 comments

It was funny. I just got an email from credit karma and checked my credit score not 5 minutes before reading your post. It said my score was 815. And that is without ever running a credit card balance and having no mortgage on my house and zero debt. We just pay all our bills on time every time. Great info!

That first one… Why do people think they need to pay money to have a decent score? There’s even companies that will loan you money just so they can report your payments to the credit bureau. This is totally not necessary, counterproductive, even!