In an ideal world, we wouldn’t need any creative ways to save money. Because we’re all grown-ups who can definitely control ourselves…right?

Whether it’s hiding candy from yourself or promising yourself only five minutes more on the treadmill just to make it through your workout (then five minutes more, then five minutes more…), our brains sometimes need a bit of a kick to do the right thing.

Why we often need creative ways to save money

It’s super weird if you think about it.

After all, we all know we have to save money! And we’re all adults doing adult things every day!

So why does logic suddenly fly out the window when it comes to our savings – or lack thereof?

Acknowledging that our self-control might need some work isn’t a bad thing – and neither is doing some sneaky little tricks to get around that fact.

Of course, ideally, we would all save the required amount and not buy anything unnecessary.

But when reality gets in the way of that, then you should definitely consider implementing some of these tips and tricks in your life.

And before you know it, you’ll be a finance ninja!

1. Have a coin jar

Remember when you would put your change into a jar and only use it once the jar was full?

Well, why not continue using this strategy when it actually works!

That extra $100 or so per year may not sound like much, but you won’t even realise you’re missing those few extra cents here and there until you add it up.

And it’s a far better use of that money than losing it between the cushions!

2. Round it up

Some banks, such as Bank of America, have a program that rounds your expenses up to the nearest dollar and then transfers the difference to your savings account.

For example, if you buy something for $8.73, $0.27 would be transferred into your savings. It’s such a small amount each time that you won’t even notice, but it quickly adds up to make a real difference to your savings rate!

And if you don’t have an account with a bank that offers this, you can always do it yourself.

Just log in to your account, check how much you’ve spent that day then transfer the difference to the nearest $1 to your savings account. Make sure that your checking and savings accounts are either with the same bank or don’t incur any fees for transfers between them.

Want to really accelerate your savings? Try rounding up to the nearest $10 and saving the difference!

(This sounds like a pain but it easily takes less than one minute. Log in, check your transactions for the day, calculate the difference, transfer. Boom, make it rain.)

3. Make money while doing nothing at all

Ever find yourself sitting on your couch aimlessly scrolling through Facebook while the TV is on and realize that you’re not paying much attention to either?

Maybe you have to spend time waiting in the car for the kids to finish soccer practice? Or perhaps you spend your commute to work wandering virtually around Pinterest?

(Hopefully, if you’re doing that last one, you’re taking the bus rather than driving yourself…)

So instead of spending your time in that way, why not use the time to make some money?

And to see just how to do this, check out 9 SURVEY SITES TO MAKE MONEY ONLINE AND EARN SEVERAL HUNDRED DOLLARS EACH MONTH.

These are some amazing survey sites that, for simply answering a few questions or watching a video, allow you to earn anything from a couple of bucks to $50 per survey.

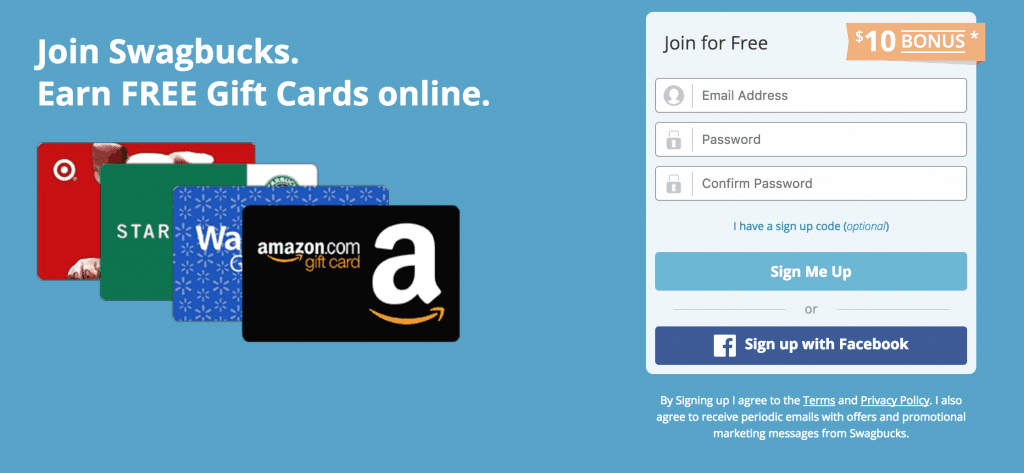

If you’re just getting started with this, I’d really recommend starting with Swagbucks.

It’s easily the most well known of all of the survey sites with a TON of ways to make some extra cash through gift cards.

(You can even earn PayPal gift cards, which are the equivalent of just getting straight up money!)

Signing up takes literally two minutes – seriously, check out the picture below for how easy it is.

And, if you sign up through this link, you’ll get a $10 sign-up bonus!

4. Make money while you shop

There are a bunch of sites that allow you to make money simply while shopping. It doesn’t even matter if you shop online or in brick-and-mortar stores – there’s always a way for you to make some cash back.

CHECK OUT THE SITES HERE: 12 EFFORTLESS WAYS FOR YOU TO MAKE MONEY WHILE SHOPPING

It helps that they’re super simple to use. After the initial registration, which often gives you a $5 or $10 sign-up bonus (every little bit counts!), you simply go to the site when you want to shop online to take advantage of some seriously great cash back deals.

With a few clicks, you can save yourself usually around 5% to 10% per store – and sometimes even up to 30%!

And as an added bonus, it can all be done automatically.

For example, Ebates has a browser extension that you can install after you’ve signed up.

Whenever you buy something online, it will automatically recognise the cash back deals that are available and apply them to your account.

This means that you can make money back without doing anything at all!

And as an added perk – sign up for Ebates through this link and get a $10 welcome bonus!

5. Automate your finances

This is, in my opinion, the most effective way to get your finances in order without spending any time or effort.

I’ve discussed before on this site how you should pay yourself before paying others and this is a great way to make sure that you’re assigning money to your savings before your other expenses. Automating your finances also goes a long way to getting your debt under control as well as avoiding any accidental late fees.

Let’s just say that it’s pretty much the black belt of tricking yourself to save.

MORE INFORMATION: HOW TO AUTOMATE YOUR FINANCES AND SAVE MONEY IN 3 EASY STEPS

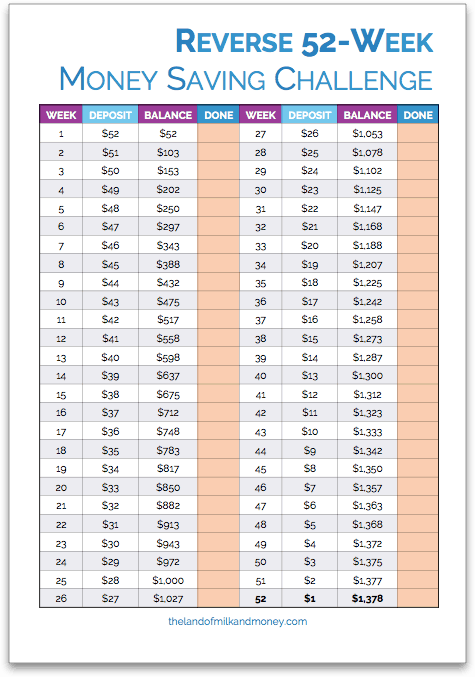

6. The week to week trick

Can you save $52 this week? Sounds a bit tough, right? Well, good news – if you’ve done that, then next week you only have to save $51! And then only $50 the week after that. Continue doing that each week for one year and, before you know it, you’ll have reached the final week in which you only have to save $1.

Want the best news? If you do that for a year, you’ll have saved $1,378 – with barely any effort at all, especially by the end!

And to make it easier for you, here’s a free downloadable worksheet to help you make it!

7. The week to week trick 2.0

If the previous trick sounds a bit, well, tricky, consider doing the following instead.

Say you want to save almost $500 per year. Each month, transfer $20 to your savings account the first week, $10 the next week, then $5 in each of the next two weeks for a total monthly saving of $40. Total amount after 12 months: $480!

Now, let’s be real – that’s a good start, but it’s not enough to make you rich. So once you’ve done it for one month and seen how easy it is, it’s time to double it.

And suddenly you’re saving $80 a month!

Just under $1,000 a year is definitely better – but can you do even better?

Consider doubling it again – or more! However much you start with in the first week, each week it will get a little bit easier until next month’s salary hits your account – at which point, the fun begins again!

Of course, you may find yourself at a point where you realise that you can, actually, save the first week’s amount each week, which is an expert level of trickery…!

RELATED ARTICLE: 19 SIMPLE MONEY SAVING CHALLENGES TO HELP YOU SAVE MORE

8. Impose your own cooling-off period

Online shopping makes it dangerously easy to spend our money with only a few clicks.

Even just popping into the mall “for one thing” can quickly cause your spending to spiral out of control.

So place your own rules on your spending habits to trick yourself into saving money.

For example, for any purchases under $100, force yourself to wait a few days before proceeding. You’ll likely find that you don’t need the item – or, if you’re anything like me, that you’re too lazy to go back to the shop to get it.

For anything over $100, consider implementing a rule that says that you can only buy the item if you wait one day per $100. Thinking of buying a new TV with that $700 you’ve wisely saved up? Wait one week before going ahead and you may realise that that $700 is way better used in your investment portfolio…

9. Get permission before purchasing

This works best if you share your finances with someone, but it could also be done with a partner with whom you have separate accounts or even a good friend who is also trying to save money.

It works like this: for any non-necessary purchases (so things like groceries are fine), make a rule that you each have to seek permission from the other before buying anything over, say, $40.

You could either call or send a message, but having to take those extra few moments to justify your spending can act as an excellent deterrent.

It can also serve as a reality check as to whether you actually need the item when your partner or friend sends back a “…really?” message after you explain why you truly need that box set of Buffy DVDs.

(I mean, obviously you do. It’s Buffy, after all.)

10. Leave your wallet at home when shopping

This is another great trick to stop extra spending!

If you’re going to the mall for something to do or to “check out a sale” or something else as equally dangerous to your budget, consider leaving your wallet at home.

That way, if you see anything that you think you want to buy, you’ll have to go back to buy it.

And I don’t know about you, but that extra effort to go alllll the way home and then allllll the way back is often more than enough to make me realise that I don’t actually need the thing I was going to buy.

11. Remove your credit card details from online shopping sites

Much like the above, this is for those of us whose laziness can (fortunately!) get in the way of our spending.

Having your credit card information saved in websites makes it far too easy to spend online.

Instead, remove these details to force yourself to think about if it’s really worth the hassle of having to find your credit card and enter the numbers (and there really are so many numbers…) before being able to buy the item.

Who knew that laziness could be so valuable!

12. Save your savings

Have you ever looked proudly at the bottom of your receipt where it tells you how much you’ve saved from either coupons or in-store sales?

So why not give yourself an additional pat on the back by saving what you’ve just saved!

All you have to do here is take the amount that the receipt says that you’ve saved and immediately transfer that amount from your everyday account to your savings account.

Try to do it as soon as possible after you’ve been shopping so you don’t forget.

This can quickly add up to hundreds of dollars saved, if not more, and the only effort it takes is a couple of clicks!

13. Save your non-spending

You could even do the same thing as in number 12 above if you’ve successfully talked yourself out of buying something unnecessarily.

Say you’re tempted by a new piece of tech but you manage to walk away.

Great job! Why not give yourself an even bigger gold star by transferring the cost of the item to your savings account?

This is doubly tricky as it can even serve as a great deterrent from buying the item in the first place if you know you’ll be using the money this way instead!

14. Save your raise

If you find yourself with a little (or big!) bump in your salary, don’t increase your spending by the same amount.

Instead, transfer your salary increase to your savings account.

You could even do this before the money reaches your account by asking your employer to transfer the difference to your 401k or, if they allow it, having part of your paycheck transferred to one account and the other part (representing your pay increase – or even more!) sent directly to your savings.

15. Save your payments

Did you just finish paying off your credit card debt? That’s truly, seriously amazing!

Now start transferring the same amount each month to your savings account instead of keeping it to spend. After all, you’ve already taught yourself how to live without that amount of money, so why not use it to your advantage!

16. Make it a competition

For my fellow people with a “healthy” competitive streak – this one’s for you.

Essentially, what you’re going to do is trick yourself into saving by harnessing your need to win.

Find a friend who’s also keen to get their spending under control then set a challenge for both of you. This could be who can save the most in a week or a goal for you both to save a certain amount of money in a month.

The person who loses (although are you really losing if you’re both saving money?) then has to do something for the other one, like bring lunch to work for them.

17. Freeze your accounts…literally

This one’s an easy trick. Simply take your bank cards and freeze them in a block of ice.

They’ll still be completely usable – unless you try to microwave the ice to make the cards defrost faster, in which case they’ll be destroyed.

Instead, you’ll have to wait for the ice to melt if you want to use them – and do you really think you can bother waiting that long to buy something you probably don’t need?

18. Turn the heater down a few degrees

Not only is this one simple as well, but it’s also great for the environment! Simply lower the heater by a couple of degrees, throw on a sweater if needed and you’ll barely feel the change – although your wallet will!

(If you’re interested in looking after the environment while looking after your finances, check out these 11 INCREDIBLE IDEAS FOR YOU TO SAVE MONEY AND SAVE THE PLANET.)

19. It’s all in the numbers

Saving for a holiday in August 2019? Make the PIN on your bank card 0819.

That way, whenever you go to use your card, you’re reminded of just how that money could be used instead.

You could do the same for your passwords on online shopping website. Say you’re aiming to retire by the end of 2025. Your password could be “Dec2025”, reminding you that each thing you buy online is one little step further away from your goal.

This trick can also be used with your regular savings. To use the holiday example, you could transfer $19.08 (i.e. 2019 + August) to your savings account each week or, with the retirement example, $122.50 (i.e. December (12) + 2025 (25)) each month.

And if you’re ever tempted to stop the transfers, just think about what those numbers represent!

20. Picture your savings

Did you know that some banks allow you to set your own picture on your bank cards? Use this to remind yourself of good savings habits by putting, say, a photo of your kids on your card if you’re trying to get out of debt.

Or, if you’re saving for a holiday, make the card a picture of your destination. If your bank doesn’t do this, you could always just wrap a photo around the card.

This is doubly effective at tricking yourself as it requires a tiny bit of extra effort in order to use the card. Those few seconds could see you realising that you just maybe don’t need the item you’re about to buy – at least not as much as what the photo represents to you.

21. Use a rewards card

Oooh, this is a simple but risky little trick.

If you’re sure you can trust yourself with a credit card that you can absolutely pay off in full each month, then consider getting a rewards card that gives you cash back whenever you use it.

That way, you won’t even realise you’re saving while you spend!

22. Make a list and check it twice

Say that you find yourself in a store about to buy a new jacket that you want…but don’t actually need.

Instead of trying to talk yourself out of buying it, add it to a list that you should carry at all times (Google Keep is a great, free option).

This list will set out all the things that you thought of buying at one point. You could even add the price of each item if you want.

You’ll soon see how much stuff you almost bought – and how much it almost cost you – as well as how quickly it can all add up.

This will show you just how much you don’t need this stuff, given that you’ve survived perfectly well without it before then.

23. Let your imagination flash you cash

Considering buying the new iPhone? I just checked and it currently costs $999.

Instead of whipping out your card, imagine someone holding $1,000 in cash – perhaps waving it like a fan towards you.

It looks like a lot of money, right? Well, that’s cause it is!

Now ask yourself if you actually need the phone – or is your current one perfectly fine as you’d rather have all that money?

It doesn’t have to only be for expensive things. Considering buying a $40 pair of shoes? Look at the shoes then imagine eight $5 bills stacked up in front of you.

Suddenly, are you sure that those shoes are actually a necessity?

24. Imagine the struggle

For this trick to work, you have to keep as little money as possible in your everyday checking account, with the rest to be kept in a harder-to-reach savings account.

This means that when you go to buy something, make yourself check your everyday account first.

Now tell yourself that’s all the money you have to spend before the end of the month.

Essentially, you’re imagining yourself as being as broke as possible. And when you’re in such a dire situation, do you really need those shoes?

25. Calculate how much it could be worth to you in future

This is something that I personally do a lot. My main financial goal at this stage of my life is to maximise my investments, so I find this to be a really effective deterrent from buying unnecessary stuff.

(Want to do the same? Take a look at THE BEGINNERS’ GUIDE TO INVESTING LIKE AN EXPERT (INCLUDING HOW TO BEAT THE PROFESSIONALS))

Let’s go back to that new iPhone. Sure, you may be in a position to spend $1,000 just like that. But think instead of how much that could be worth to you in the future!

If you’re earning a 7% annual rate of return (and you can find out how to earn way more than this for minimal risk here!), that $1,000 will have earned you $70 by this time next year! That’s $70 for doing absolutely nothing!

Want to be extra tricky? Did you know that you can easily calculate how long it will take you to double your money?

It’s called the Rule of 72, which says that the amount of time needed to double your money is equal to 72 divided by your rate of return. To take the 7% example, simply do 72/7 = 10.2. This means that it will take 10.2 years for your $1,000 to become $2,000 if invested in that way.

This may sound like a long time, but it means that you’ve earned a bonus $1,000 in 10.2 years, equivalent to $98 per year – for doing nothing!

(Do you want to know more about how this works? Check out THE ONE PRINCIPLE THAT WILL GUARANTEE YOUR FINANCIAL FUTURE.)

26. Divide your time

This is something that I used to do all the time when I was a teenager.

As a personal finance newbie back then, this is the main thing that drove me to save as much as I could from the moment that I started earning my own money.

You see, when I was a teen, I worked at McDonald’s – and loved it!

Not only was it fun (I actually mean that, there’s nothing like the adrenaline of a backed-up drive thru!) but it meant that I had my very own income.

Sure, it wasn’t as much as I’m earning from my grown-up job today, but I wanted to make every cent count.

And how did I do that?

By dividing the cost of everything I bought by my hourly salary.

That way, I knew exactly how long it had taken me to earn that money and allowed me to see whether it was actually worth it.

Say I wanted to buy those $40 shoes mentioned above. But I earned $9 an hour, which meant that it took me 4.5 hours to earn that money – not to mention tax.

I’d then think back to a particularly difficult five-hour Friday night shift after school.

Were the shoes really worth all that time and effort I’d spent? More often than not, the shoes went back on the shelf.

And with the most basic of calculations, that’s how I saved $10,000 by the time I was 18 years old!

27. Treat yourself

A treat every now and then isn’t a bad thing – as long as it’s being used to make you save more and that it doesn’t completely wipe out all the good work you’ve already done.

So if you’ve used the tricks in this article to save, say, $1,000, go and have a celebratory breakfast with friends.

Or perhaps if you find yourself having successfully saved for three months straight, why not go on a date night to the movies or buy a bottle of wine to share with your friends or partner.

After all, you’ve earned it!

2 comments

#26 Divide your time:

I did that with my first job. My BFF and I worked at the movies and made $5.25/hour. We’d go out to eat or go shopping and I’d be careful with my money. She’d spend hers a lot more easily. I would say things like oh I’m not sure it’s worth working XX hours for this item, so I’m not going to buy it. She freaked out on me eventually and told me to stop doing that and start enjoying and living life. We are still total opposites!

It’s like you’re telling my own story! My best friend is HORRENDOUS with money. She thinks I’m cheap, I think she’s nuts – and yet we’ve been friends for almost 20 years. Opposites attract, right?