The question “How much money do I need to retire?” is often seen as impossible to answer – or an impossibly large answer.

But you may be surprised to hear that it’s amazingly simple to work out and, better yet, completely possible to reach.

As long as you’re not planning to spend wildly during your retirement, the magic number for the amount of money you’ll need is likely to be much less than you think.

In addition, there’s a double bonus in getting your spending under control now in order to accelerate your saving for retirement.

Firstly, you’ll be saving more money now, allowing you to retire even earlier.

At the same time, those reformed spending habits will allow your money in retirement to last even longer.

Essentially, with one action, you’re doubling up your chances of retiring early!

And as an added bonus, it’s so easy to calculate how much you will need for retirement, even those of us who are, ahem, mathematically challenged can figure it out.

The simple formula to determine how much money you need to retire

Yes, I’m serious. Using this super straightforward formula, you’ll be able to find out just how much money you’ll need to keep you going for the rest of your life.

There are actually two different calculations you can use to work this out, both of which produce the same figure.

Based on your average annual expenditure

This is the most well-known and it’s as simple as this:

Step 1: Work out how much you will need to spend per year to live the lifestyle that you want to have during retirement. This therefore assumes that this is how much you will continue to spend every year for the rest of your life.

(Not sure how much that is? To get an idea of your current spending to base your calculation off that figure, I’d recommend trying Personal Capital. It’s a super easy way to keep track of your finances.)

Step 2: Multiply it by 25. I’ll explain why below.

Based on your average monthly expenditure

This will produce the same figure as above, but may be easier if you prefer to track your expenses on a monthly basis:

Step 1: Work out how much you will spend per month during retirement.

Step 2: Multiply it by 300. Explanation coming, I promise.

Show me how, Maths is hard

Step 1: Say I’m planning to spend $40,000 per year for the rest of my life. That’s equivalent to $3,333.33 per month.

This includes everything. Taxes (e.g. capital gains tax from selling your investments year to year, land tax or similar expenses depending on where you live etc.), living costs (including expenses relating to your residence as well as e.g. food, clothes etc.), and lifestyle costs (travel, the new hobby you plan to take up when you retire etc.).

Step 2: $40,000 x 25 = $1,000,000

Similarly, $3,333.33 x 300 = $1,000,000

So at this rate of expenditure, I would need $1,000,000 to retire.

Simple!

Any questions?

Where did you get those numbers from?

The numbers used in these calculations are taken from what’s known as the four percent rule.

This is based on an assumption that the average annual rate of return on your investments will be 5% after inflation.

Consequently, this allows you to safely withdraw 4% of your investments forever without your money running out. This is, however, subject to some basic money management on your part.

*whisper* Um, what’s inflation?

While some of you may know this already, I have been asked to break this down by a few others, so this section is for the latter group.

Inflation is the rate at which the general level of prices of goods and services is rising. This means, at the same time, the amount of things that your money can buy is decreasing at the same rate.

For example, at an inflation rate of 3%, $1,000 last year (if it does not earn any interest) will be able to buy $970 worth of things this year.

This is partly why you should make your money work for you to ensure that it keeps rising ahead of the rate of inflation and thus gains, rather than loses, value.

(Not sure how to do that? Why not check out The Beginners’ Guide To Investing Like An Expert (Including How To Beat The Professionals).)

It’s also why keeping all of your money in a standard bank account with low interest rates (or, say, under the mattress) is not sound investment advice: because it will lose value from year to year.

Got it? Cool. Let’s keep going then, shall we?

How do you know that this actually works?

Because smarter people than me did the calculations.

Enter the Trinity Study.

The Trinity Study was first published in the late 1990s and essentially asked: “If you had retired at anytime since 1926, how much could you spend each year for 30 years without running out of money?”

It’s pretty detailed and super interesting. Well, at least I think so. (Ready to invite me to your next party yet?)

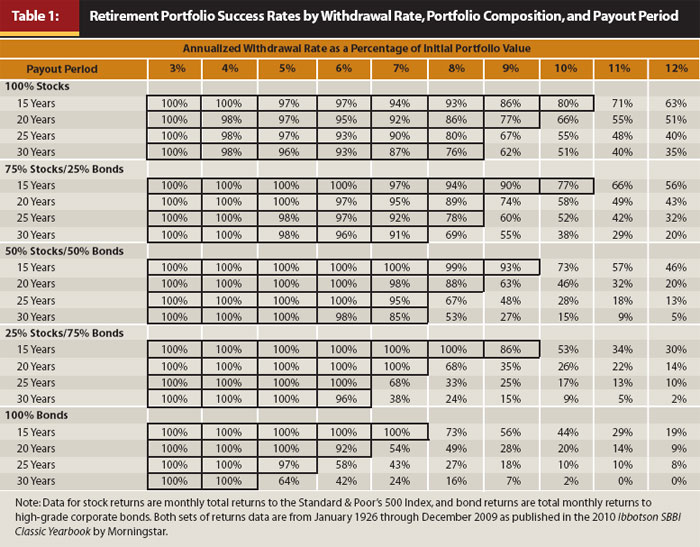

As a summary, some key conclusions to take from it (as can be seen in this table) are as follows:

{kind=link}

- If you withdraw 4% or less of your portfolio value each year, you are pretty much guaranteed to be able to live off your investments for 30 years. This is especially the case if you hold 75% stocks and 25% bonds.

- Not sure what a bond is? Check out our summary here!

- If you would prefer to withdraw 5% or 6% of your portfolio value each year, it is best for you to hold 50% stocks and 50% bonds.

- If you are considering withdrawing 7% or more of your portfolio each year, it becomes less likely that you’d be able to make it to the end of the 30-year period. BUT it’s not impossible, as long as you keep a good eye on things and are prepared to adjust your spending if the market falls.

This means that if you commit to only withdrawing 4% of your portfolio value per year, it is as close to certain as you can get that you would be able to fund your lifestyle for thirty years without earning an additional cent.

But will this continue to be true for the future?

Almost certainly.

What about future market crashes?

The 30-year periods looked at by the Trinity Study included some of the biggest stock market crashes in history, including the Wall Street Crash of 1929 and Black Monday in 1987. And it still found that you could live for 30 years off a withdrawal rate of 4%.

That said, there are things to keep in mind.

For example, if you happened to be unlucky enough to retire in 2008 as the market crashed and your portfolio value similarly plummeted, you would have had to limit your spending a bit until the market recovered.

(As it always does, mind you. After the biggest drop in any single day in history in 2008, the markets recovered to the same pre-crash point after 4.5 years. A good lesson for why you shouldn’t panic sell during the next dip.)

This is because while 4% of $1,000,000 is $40,000, if your portfolio suffers a drop of 20% to $800,000, then 4% of that would only be $32,000. In cases like that, it would be best to reduce your spending accordingly during the downturn to stay at the 4% safe withdrawal rate for that year.

Taking the example above of retiring in 2008, it should be noted that this aligns with what Wade Pfau has found with respect to the 4% rule:

“Retirement success is more dependent on what happens early in retirement than late in retirement. In fact, the wealth remaining 10 years after retirement combined with the cumulative inflation during those 10 years can explain 80 percent of the variation in a retiree’s maximum sustainable withdrawal rate after 30 years.”

If your eyes glazed over at that, don’t worry, I got you.

To break it down: If you get through the first ten years of your retirement with your investment portfolio still at a reasonable amount (i.e. you spend an amount equivalent to your safe withdrawal rate each year and inflation doesn’t suddenly sky rocket), then you’re essentially guaranteed to make it the rest of the way.

As such, any blips during those first ten years may have to be carefully managed, depending on the severity of the blip. But assuming you make it through – and chances are very high that you will – you’re pretty much good to go.

Is there anything that the Trinity Study didn’t consider?

Glad you asked!

The Trinity Study made some fairly broad assumptions, such as the following:

You won’t earn any money from working during retirement. We’ve already clarified though that this isn’t true for almost half of the population.

You won’t gain money from any other sources during retirement, such as through inheritance or social security. While social security in most developed countries is not expected to be provided at the same level in the future as it has historically, you are still likely to receive a small amount of income from this.

You won’t adjust your spending during downturns. This is more than likely incorrect given that most people would normally make small adjustments as needed during more difficult times.

You won’t naturally spend less as you age. Not true, as it’s been established that people spend less as they get older. Check out Table 2 at that link, which indicates that people, on average, have annual expenditures at age 75 and up of less than half of those aged 55-59.

All of this means that it is highly unlikely that you will not earn another cent during retirement.

And any money you earn during this time reduces the amount that you have to withdraw from your investments in order to have on hand the funds that you need in a particular year to pay for your lifestyle.

(For example: if you have calculated that you need to withdraw $40,000 from your portfolio each year but then you earn $5,000 from other sources in a particular year, you will ultimately only need to withdraw $35,000 that year to fund your lifestyle)

This, in turn, allows your investment portfolio to last even longer.

Does this mean that my money will run out after 30 years?

It’s true that the Trinity Study calculated the 4% rule based on its study of multiple 30-year periods.

However, people live longer now.

More importantly, those of us who intend to retire early will need our investments to last significantly longer than 30 years.

But let’s revisit the assumption that was made at the time of establishing the 4% rule:

“This is based on an assumption that the average annual rate of return on your investments will be 5% after inflation.”

As such, withdrawing 4% of your investments each year (with any adjustments as needed during economic downturns), will mean that you will be withdrawing less than your portfolio’s returns. This, in turn, means that your money should last forever.

So what’s the biggest risk to my ongoing financial independence using this formula?

Subject to you ensuring that your spending does not get wildly out of control relative to your investments, the biggest issue is that you may have too much money leftover when you die.

This article points out the following:

In fact, not only do 90%+ of retirees finish with more than their starting principal after 30 years by following the 4% rule (so even if you outlive the time horizon, there’s still funds left over), the “typical” retiree actually finishes with many multiples of their starting wealth with this spending approach! Over 2/3rds of the time the retiree finishes with more-than-double their initial principal left over. And the median wealth at the end of 30 years is almost 2.8X principal! One-in-six scenarios finish with more than quintuple the retiree’s initial wealth!

How irritating if I check my account in my 90s and see that I still have more than $1,000,000 left – imagine how much earlier I could have stopped working!

This is obviously not the worst problem in the world to have. But still.

(Please don’t take this as meaning that the 4% rule is rubbish and that you can spend whatever you want. My “irritation” at having more than $1,000,000 left is nowhere near to the “irritation” I would have if economic conditions changed and I ran out of money as a retiree.)

Summary

In brief, you should keep the following in mind when determining when (and how) you can retire early:

- To calculate the amount of money you need: multiply your annual expenses by 25 OR multiply your monthly expenses by 300

- If you withdraw 4% or less of your investment value per year, you are almost guaranteed to be able to fund your lifestyle forever. Even 5% to 6% should be fine, subject to slight adjustments to the percentage of stocks and bonds in your portfolio

- Make sure you cut back your spending as needed during economic downturns

- If you earn any money at all during your retirement, as most people do, this will allow you to withdraw even less from your investments, thus further ensuring the success of the 4% rule as a retirement strategy