Welcome to the Step-by-Step Guide to Investing Like a Pro! This post is Step 1 of a Guide that we believe will give you all the information you need to set up an investment portfolio that can see you through the rest of your life.

It’s extremely simple, very cheap and the risks are minimal. Better yet, it will, over time, give you returns on your investments that the vast majority of professionals can only dream of achieving.

You may think it sounds too good to be true. I assure you, it’s not.

The process of investing is often made to sound far too scary and complicated for you or me to do on our own, without the so-called expertise and subsequent cost of a “professional”.

But I want to show as many people as possible that this is absolutely not true. You can most definitely do it on your own and see great returns for a very low cost.

Here’s how.

Investing is only for experts, right?

A key aspect of reaching financial freedom is making your money work for you. After all, allowing your money to grow through effective investing will allow you to reach your magic retirement amount that much quicker.

This can be easier said than done for many of us. Often it can seem like the only way to do this is to pay a small fortune to a financial advisor who will throw some impressive-sounding numbers at us. Then, if we agree with their proposed strategy, we find ourselves continuously shelling out more money for their services – without really knowing why we’re doing so.

Blindly shovelling money in one direction (insert boy band pun) just because a so-called expert told you to do so is no way to spend your hard earned income. And it’s no way to secure your wealth.

Actually, investing is very simple

Instead, I’m going to explain to you just how simple investing can be.

In particular, you may be surprised to hear that the method that has seen the best returns over time is both one of the cheapest and simplest ways to invest your money.

You don’t need the services of a financial advisor. With just a few clicks, you’ll be on your way.

You don’t need to spend a small fortune. With an annual fee that you’ll barely notice, you’ll be seeing returns that are next to impossible in other asset classes.

You also don’t need to spend hours of your time researching company information. (You’re welcome, by the way – those are not the most exciting documents in the world to read.)

It also doesn’t involve guessing just which areas of the market will perform the best for you in the coming years. Simply set and forget – well, for the most part.

And considering that one third of all assets in the US are following this same investment strategy, this is clearly a method that is considered trustworthy by a large chunk of the investing population.

I will say this upfront: please note that I am not a financial advisor. You should always do your own research before committing to any investment. (More information can be found in the Disclaimer.)

This is, however, the way that I invest my money, along with many, many other people. Given the sheer amount of money being invested in this way, this is clearly a method that is considered trustworthy by a significant portion of the investing population.

As such, it is definitely worthy of your consideration.

Where do I start?

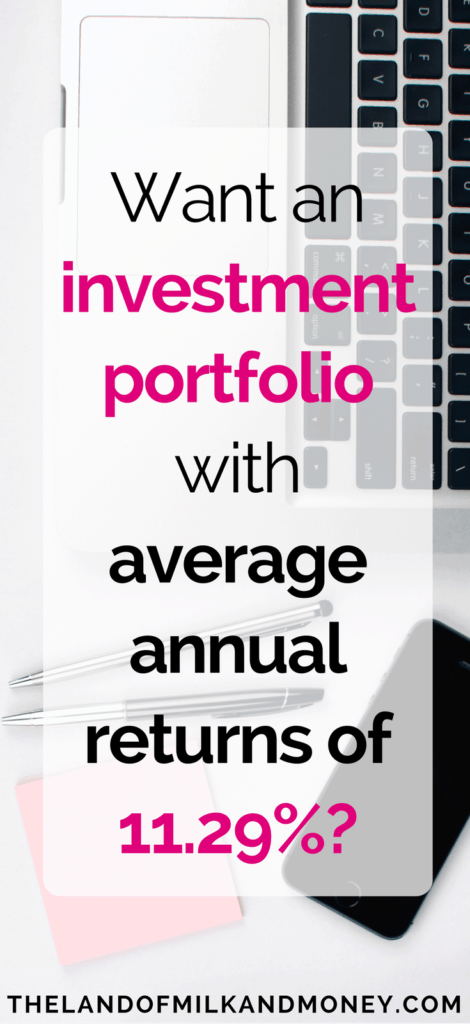

Firstly, we need to pick the type of investment that has consistently had the best returns.

How about one where the returns look like this?

Don’t be fooled by some of those scary-looking dips. Incredibly, this represents an average annual rate of return of 11.29%, calculated from 1950.

To be fair, this doesn’t consider inflation, which would bring the average annual rate of return down to a still very healthy 7.19%.

Whichever way you want to look at it: it’s your money working damn hard for you.

I’m talking, of course, about the stock market – the investment class that has had, hands down, the best returns over time.

Despite this, people get a bit funny when you say the “S” word. They imagine the stock market as being exclusively for men (come on, you all pictured a man) in dark suits yelling at each other as numbers flash on endless rows of screens and jagged lines plunge menacingly above their heads.

But what if I told you that there’s a way to take advantage of these incredible returns that

- Doesn’t require you to be a yelling man in a dark suit (congratulations, ladies!);

- Doesn’t require you to do much of anything, really;

- Is recommended as the most consistent way to see these kinds of returns by millionaires the world over; and

- Is extremely low cost?

Welcome to the magical world of index funds!

What is an index fund?

Simply put, an index fund is an investment fund that holds all the stocks (or bonds – we’ll get to them later) of an index.

And what’s an index? It’s essentially a list of investments.

See that graph at the start of this article? It’s tracking the performance of one of the most common indices, the Standard & Poor’s 500, known as the S&P 500.

The S&P 500 consists of some of the largest companies in the US, the list of which can be seen here. To give you an idea of the type of companies that form the S&P 500, the top five by weight at the time of writing (source) are Apple, Microsoft, Amazon, Facebook, and Johnson & Johnson.

This isn’t the only major index. For example, you may have heard of the Dow Jones Industrial Average. However, the S&P 500 is probably the most well known and will be the one most commonly referred to on this website.

Accordingly, an index fund that tracks the S&P 500 index owns the same stocks as those that form the S&P 500.

The logic behind this is a belief that tracking the market’s performance will produce a better result than actively managed funds.

And in the vast majority of cases, this has turned out to be entirely correct.

Wait, what’s an actively managed fund?

Have you ever been discussing your finances with your friendly neighbourhood bank manager and they’ve whipped out a shiny piece of paper with green lines marching optimistically upwards?

And then they’ve proceeded to tell you how great their institution is for your money? That they’ve picked the Best Stocks Ever™ and all you have to do is put your money in their fund and they’ll make you rich beyond your wildest dreams?

Firstly, sorry to break the news to you, but they’re (highly probably) wrong. We’ll cover why below.

But in any case, that’s an actively managed fund.

This type of fund includes most mutual funds. It means that a fund manager has used his/her skills and knowledge (or “skills” and “knowledge”) to try to pick the stocks that will perform the best.

The fund manager’s job doesn’t end there. He or she will have to do research on these stocks, spend time buying and selling, consider the tax implications of such transactions etc.

In sum, all of this time and effort costs money. And this leads to the fees for actively managed funds being higher.

On the other hand, passively managed funds simply seek to match the returns of the part of the stock market that it has chosen to follow.

Just set and forget. That is, set the index that the fund should follow. Then forget in that you don’t touch it – it just continues on its merry march in line with the market.

But why would I want to simply match the market when I’ve been told that I can beat it?

Because it’s highly unlikely that you – or your chosen fund manager – can do that.

According to The Wall Street Journal, “more than 90% of active managers underperformed their benchmark indexes over a 15-year period”, calculated to the end of 2016.

That is, in more than 90% of cases, actively managed funds produced worse returns than passively managed funds that track an index.

Want some more specific numbers?

Marketwatch observed the following based on a report issued by Standard & Poor’s using figures from up to the end of 2016:

“Over the last 15 years, 92.2% of large-cap funds lagged a simple S&P 500 index fund. The percentages of mid-cap and small-cap funds lagging their benchmarks were even higher: 95.4% and 93.2%, respectively.

In other words, the odds you’ll do better than an index fund are close to 1 out of 20 when picking an actively-managed domestic equity mutual fund.”

This is only further confirmed by looking at results from even further back in time. As per this Freakonomics podcast:

“If we go back to 1970, we find that there were approximately 400 funds in business and basically 330 or [3]40 have gone out of business. It turns out, in that period, there were two mutual funds who beat the market by more than two percent per year. Two! That’s half of one percent of all the funds that started in the business. Those are your odds.” – Jack Bogle

(Remember that name: Jack Bogle. He’ll pop up again shortly.)

So we’ve established that, in the vast majority of cases, even the so-called experts can’t pick winning stocks.

Of course, some fund managers or day traders have a lucky day/year and may beat the market. But there is no way that they are able to see those same results year in year out.

Especially compared to the strategy of simply buying and holding an index fund.

It’s also extremely unlikely that you’ll stumble across the specific fund manager that is able to do this year on year.

Sure, you may get extremely lucky. But when we’re talking about your entire life savings and the rate at which you’ll be able to be financially free, do you really want to risk it?

Instead, if you had the option of putting your money in an investment type that performed better in more than 92% of cases, wouldn’t that be the one you’d go for?

There’s also another issue with actively managed funds that needs to be mentioned.

The cost of actively managed funds is destroying your returns

As mentioned above, actively managed funds require, unsurprisingly, active management.

That is, someone – or a team of someones – is selecting just which companies’ stocks should form your fund. They are undertaking research and buying and selling based on their findings, all of which take time and (supposedly) expertise. This, in turn, all costs money.

These costs are covered through the management fees charged to you, the investor. Typically, these fees will be around 1.3% – 2.5%.

At the same time, the management fees for an index fund are always much lower. For example, Vanguard (another name to keep in mind) states that its average fee is 0.12%

This may not seem like a significant difference. However, the effect of this on your portfolio over time can be massive. Let’s look at the following as an example:

Homer decided to invest $100,000 with Lionel Hutz Investments Ltd. Mr Hutz promised annual returns of 7% for the low fee of 1.3%.

Marge, on the other hand, chose to invest her own $100,000 in an index fund that tracked the S&P 500, with fees of 0.04%.

(If you want to be really tricky and see why I’ve used that specific percentage, check out Step 4 of the Step-by-Step Guide to Investing Like a Pro: The Simplest Investment Portfolio You Will Ever Need)

Given that this is tracking the market average, Marge will also have returns of 7% after inflation.

Already, Marge is in a better position. After all, her effective rate of return, after deducting management fees, is 6.96%. Homer, however, is receiving an effective rate of return of 5.7%.

So how do each of their $100,000 investments look after 20 years?

Homer ends up with $303,040, which isn’t bad. But Marge, with her low-cost index fund, ultimately has $384,085.

That is, she is more than $80,000 better off. Put another way, Homer has ultimately spent just over 80% of his initial investment on excess management fees.

(Hmm, I wonder why investment bankers are so rich…)

We’ve discussed before on The Land of Milk and Money how imperative compound interest is to building your wealth. This example only further reiterates that point.

As you can see, even a fraction of a percent difference in fees can affect your wealth enormously.

Consequently, for an actively managed fund to perform better than an index fund, not only do they have to beat the market. They also have to exceed market returns by several percentage points to make up for their own returns being partly eaten away by significantly higher management fees.

“But wait!” I hear you exclaim. “Why bother paying fund managers all that money if they can’t get me the same – or even better – results than the market?”

Why, indeed!

Summary

To summarise so far: in the vast majority of cases, index funds perform better and cost less.

If you want to make your money work for you – and you should – then they are absolutely the best way to go.

Ahh, but we’re not done yet, right? You’re a savvy investor-in-training so you, of course, need more information before making any big decision on your financial future.

So check out Step 2 of the Step-by Step Guide to Investing Like a Pro: How To Invest Your Money For The Best Returns (For The Least Amount Of Cost and Effort).

Read the entire Step-by-Step Guide to Investing Like a Pro here:

Step 1: The Beginners’ Guide To Investing Like An Expert (Including How To Beat The Professionals)

Step 2: How To Invest Your Money For The Best Returns (For The Least Amount Of Cost and Effort)

Step 3: How To Prepare For Risks To Your Investments – And Turn Them Into Rewards

Step 4: The Simplest Investment Portfolio You Will Ever Need

Step 5: Why Bonds May Save Your Life (Or At Least Your Portfolio)

Step 6: How To Build Your Very Own Expert Investment Portfolio